Quicklinks to page section:

- Schools... the primary recipient of property taxes

- Spending per pupil and school ratings

- vs. Private school tuition

- School District Policy on Proof of Residency

- Survey of School leadership, teachers, culture

- ISBE Staff count discrepancies

- Student enrollment vs. staff count

- PARCC Exam scores

- Administrator Contracts, Benefits and Pensions

- Penalties Imposed on Taxpayers by Districts

- Teacher Benefits and Pensions

- School Pension/OPEB Liabilities

- Teacher pension vs. Social security

- Mapping the $100,000/year teacher pensions

- Top 5 highest paid teachers in each District

- Districts are nontransparent on not-for-profits

- School contracts shrouded in SECRECY

- Compare pensions by State

- The great American Ponzi scheme

- Restructure benefits and save millions

- School funding and funding reform

- Ideas to implement

- Tinley Park is no Silicon Valley

- Summary of Questions

- Taxpayers get it

- Articles to read

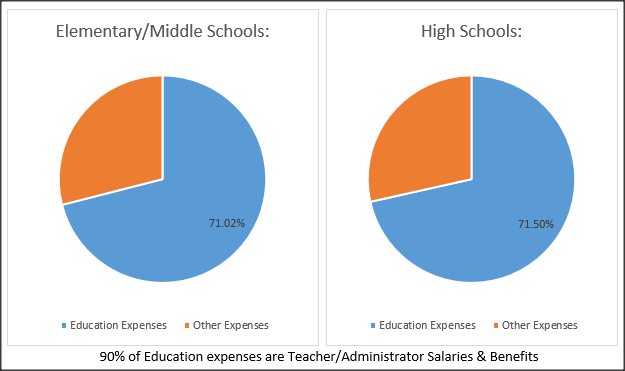

Schools... the primary recipient of property taxes

Where oh where do our tax dollars go?

About 29% of "other expenses" is listed on school expense reports as overhead, maintenance, transportation, etc. Of the 71% of earmarked "education expenses" 90% is teacher and administrator salaries and benefits. The remaining 10% is spending for students?

Spending per pupil & school ratings

Elementary districts

District 140

Instructional Spending per student: $7,140 Operational Spending per student: $11,061 John A. Bannes Elementary School, Rated 9/10 Fernway Park Elementary, Rated 8/10 Helen Keller Elementary School, Rated 8/10 Christa McAuliffe Elementary, Rated 8/10 Millennium Elementary, Rated 9/10 Virgil Grissom Middle School, Rated 8/10 Prairie View Middle School, Rated 8/10 District 145 Instructional Spending per student: $5,406 Operational Spending per student: $10,564 Arbor Park Middle School, Rated 6/10 Kimberly Heights Elementary, N/R Morton-Gingerwood School, N/R Scarlet Oak School, Rated 4/10 District 146 Instructional Spending per student: $9,105 Operational Spending per student: $15,272 Central Middle School, rated 6/10 Fierke Education Center, rated 5/10 Fulton School, rated 6/10 Kruse Education Center, rated 8/10 Memorial Elementary School, rated 5/10 District 159 Instructional Spending per student: $7,435 Operational Spending per student: $15,251 Marya Yates School, Rated 6/10 District 161 Instructional Spending per student: $5,722 Operational Spending per student: $10,601 Hilda Walker Intermediate, Rated 7/10 Summit Hill Junior High, Rated 7/10 Dr. Julian Rogus Elementary, Rated 7/10 Arbury Hills School, Rated 5/10 |

High School districts

District 210

Instructional Spending per student: $7,023 Operational Spending per student: $13,225 Lincoln-Way North High School, Rated 10/10 Lincoln-Way East High School, Rated 10/10 District 227 Instructional Spending per student: $9,247 Operational Spending per student: $18,407 Rich South High School, Rated 3/10 District 228 Instructional Spending per student: $8,915 Operational Spending per student: $14,622 Tinley Park High School, Rated 5/10 District 230 Instructional Spending per student: $9,259 Operational Spending per student: $15,043 Victor J. Andrew High School, Rated 8/10 Carl Sandburg High School, Rated 9/10 Can the schools provide taxpayers with a breakdown of costs that equate to the total "Spending Per Student" which they report? As a parent with a student in District 146 I wonder why I am always asked to donate, contribute money to the PTA and other school activities, and why I am required to purchase supplies for the classroom and teacher before the start of a school year. Where does the school allocate the "Spending Per Student" funds?" - Concerned District 146 Parent |

vs. Private School tuition...

Should taxpayers receive vouchers to send their kids to private school?

- ***Multi-student discounts are available at each private school***

- Saint George Catholic School, $5,592 tuition

- Marian Catholic High School, $9,975 tuition

- Brother Rice High School, $10,700 tuition

- Marist High School, $11,500 tuition

- Mother McAuley High School, $10,650 tuition

- Providence Catholic High School, $11,150 tuition

- Chicago Southwest Christian Schools, Cost not available online

Sources indicate that the value of a private education exceed a public school education.

- Private School Report Cards

- At the spending per student that public schools are reporting, why are private schools providing a better education at their tuition rate?

- Why aren't public school teachers and administrators compensated based on performance like every other job?

School District Policy on Proof of Residency

After seeing an article about Orland Park District 135 beginning to need proof of student residency in 2017, we wondered when proof of residency stopped being required and what Tinley Park school district policy was on student residency. Tinley Taxpayers reached out to the Superintendent of each school district serving Tinley Park residents. On December 20, 2016 we asked them "Does District XYZ require proof of residency each year at school registration? This article about District 135 has us wondering if District XYZ requires the same documentation: http://patch.com/illinois/orlandpark/orland-school-district-135-require-proof-residency-each-school-year"

Here are the district responses:

District 140

12/21/16 "Good morning...we require proof of residency at registration. It's required at initial registration."

District 145

1/5/17 "Like all school districts, verification of residency is an important mandate for our schools and community. Please see our web site (www.arbor145.org) for registration information for returning students and for students who are new to our district. Students are required to register each school year. Also, student residency is verified each year for everyone through the US mail. We also monitor and re-verify during the year when appropriate. District 145 remains committed to investigating all cases of question along with retrieving out of district tuition fees. My administrative team renews/reviews our registration process each year. We also consult and meet with other districts."

District 146

D146: 12/21/16 "Yes, the District does check residency prior to registration. Feel free to let us know if you have any other questions! Thanks."

TTU replies: 12/21/16 "Is this an annual procedure or just at the time of first/new registration?"

D146: 12/22/16 "Residency checks are ongoing throughout the school year. The District works with the USPS to confirm addresses, neighbors and citizens who have tips, and uses additional investigative means when necessary."

District 159

D159: 1/5/17 "Yes"

TTU replies: 1/6/17 "We're looking for your actual residency procedure, i.e. if District 159 verifies residency annually, what is required as proof of residency, etc."

D159: Awaiting response

District 161

12/22/16 "Yes, District 161 requires similar residency documentation for students new to the district. In a review of the list of documents presented in the news story, District 161 is more restrictive in Category B. For returning students who must re-register each year, the District utilizes full residency disclosure and/or checks of residency status through its LexisNexis public record software. Please let me know if you have further questions. Sincerely, Supt. Barb Rains

Here are the district responses:

District 140

12/21/16 "Good morning...we require proof of residency at registration. It's required at initial registration."

District 145

1/5/17 "Like all school districts, verification of residency is an important mandate for our schools and community. Please see our web site (www.arbor145.org) for registration information for returning students and for students who are new to our district. Students are required to register each school year. Also, student residency is verified each year for everyone through the US mail. We also monitor and re-verify during the year when appropriate. District 145 remains committed to investigating all cases of question along with retrieving out of district tuition fees. My administrative team renews/reviews our registration process each year. We also consult and meet with other districts."

District 146

D146: 12/21/16 "Yes, the District does check residency prior to registration. Feel free to let us know if you have any other questions! Thanks."

TTU replies: 12/21/16 "Is this an annual procedure or just at the time of first/new registration?"

D146: 12/22/16 "Residency checks are ongoing throughout the school year. The District works with the USPS to confirm addresses, neighbors and citizens who have tips, and uses additional investigative means when necessary."

District 159

D159: 1/5/17 "Yes"

TTU replies: 1/6/17 "We're looking for your actual residency procedure, i.e. if District 159 verifies residency annually, what is required as proof of residency, etc."

D159: Awaiting response

District 161

12/22/16 "Yes, District 161 requires similar residency documentation for students new to the district. In a review of the list of documents presented in the news story, District 161 is more restrictive in Category B. For returning students who must re-register each year, the District utilizes full residency disclosure and/or checks of residency status through its LexisNexis public record software. Please let me know if you have further questions. Sincerely, Supt. Barb Rains

|

District 210

12/21/16 "Here is the residency verification that is part of annual registration. Any student that does not directly come from a feeder district must provide verification of address similar to what was stated in the article. Any student who moves within the district once enrolled must also verify their new address. Hope this helps." |

|

District 227

No response as of 2/13/17

District 228

12/21/16 "We require proof of residency for all new and freshmen students."

District 230

12/21/16 "HI, Thank you for writing to seek information about District 230's Annual Residency Verification process. You will find the details in this news article on the school website. http://andrew.d230.org/all-district-230-students-must-prove-residency-within-the-district-each-year/. District 230 believes this is an important process to follow each year out of respect for the taxpayers who support our district as well as for the students who attend our schools. Thank you"

No response as of 2/13/17

District 228

12/21/16 "We require proof of residency for all new and freshmen students."

District 230

12/21/16 "HI, Thank you for writing to seek information about District 230's Annual Residency Verification process. You will find the details in this news article on the school website. http://andrew.d230.org/all-district-230-students-must-prove-residency-within-the-district-each-year/. District 230 believes this is an important process to follow each year out of respect for the taxpayers who support our district as well as for the students who attend our schools. Thank you"

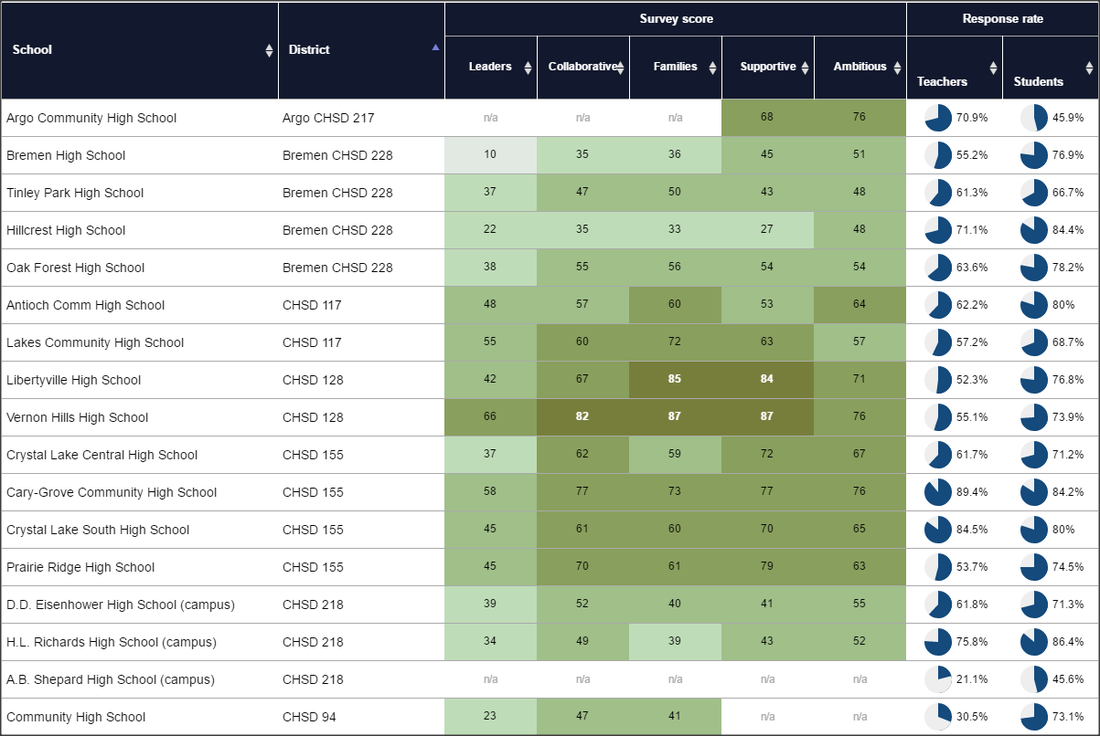

Survey of School leadership, teachers, culture and atmosphere

|

The Illinois State Board of Education recently made public the results of the 2015 "5 Essentials Survey," a compilation of responses from about 675,000 students and 103,000 teachers that reveals the strengths and weaknesses affecting school culture and atmosphere.

The survey, overseen by UChicago Impact, a University of Chicago nonprofit organization, is intended to measure categories that relate to successful schools. These ingredients for success, stemming from decades of research at the University of Chicago, are the five essentials: effective leaders; teachers who collaborate and commit to a school; strong relationships with families and communities; a safe and supportive atmosphere; and challenging and engaging instruction. The Tribune found that in four of the five areas, only about a quarter to a third of schools scored high enough to be considered strong, raising questions about whether schools are creating the kind of environment that allows students to learn and improve. Search for your school by typing the school name, district or county in the link below. |

|

Staff count discrepancies...

Per section 10-20.47 and 34-18.38 of the School Code [105 ILCS 5/10-20.47 and 5/34-18.38] require school districts to report administrator and teacher salary and benefits to the Illinois State Board of Education (ISBE). We found that documents that the school boards posted to their district websites have in many instances grossly under-reported teacher/administrator employee counts.

For instance...

Locating actual staff counts at Tinley Park elementary schools was a bit more challenging and we are still researching actual staff counts versus the ISBE report counts.

A discrepancy of teacher/administrator counts and salaries amounts to tens of millions of dollars that is not appearing on the school district reports to the ISBE and the public.

It is hard to believe that the discrepancy of "staff" listed on school websites (vs. the ISBE reports of admin/teacher count and salary) is due to office, custodial, maintenance and other workers. These are large discrepancies. Furthermore, after reviewing the ISBE teacher/admin salary reports, it was apparent that there are no reporting standards, at least in the Tinley Park School Districts' salary reports. Each report has different salary breakdowns and some district reports look less complete than other districts. If this is just 1 report at the local level in Tinley Park showing lack of uniformity, it's scary to think how bad the other reports are.

School Districts should be required to file and provide to the public, standard/uniform reports and documentation with data required by the ISBE each year. The lack of uniformity in the publicly provided ISBE salary and teacher count reports in just Tinley Park School Districts alone are evidence of a much needed reform in school reporting procedures. Just as taxpayers and businesses file standardized reports with the IRS and State, the ISBE should also require uniformity in reporting. This would allow for quicker and more efficient review and AUDITING.

For instance...

- District 210: Reports 463 total administrators and teachers between 4 schools, but the staff report on (4) school websites total 567 staff. A difference of 104.

- District 227: Reports 255 total administrators and teachers between 3 schools, but the staff report on the (3) school websites total 665 staff. A difference of 410.

- District 228: Reports 338 total administrators and teachers between 4 schools, but the staff report on the (4) school websites total 549. A difference of 211.

- District 230: Report 567 total administrators and teachers between 3 school, but the staff report on the (3) school websites total 829. A difference of 262.

Locating actual staff counts at Tinley Park elementary schools was a bit more challenging and we are still researching actual staff counts versus the ISBE report counts.

A discrepancy of teacher/administrator counts and salaries amounts to tens of millions of dollars that is not appearing on the school district reports to the ISBE and the public.

It is hard to believe that the discrepancy of "staff" listed on school websites (vs. the ISBE reports of admin/teacher count and salary) is due to office, custodial, maintenance and other workers. These are large discrepancies. Furthermore, after reviewing the ISBE teacher/admin salary reports, it was apparent that there are no reporting standards, at least in the Tinley Park School Districts' salary reports. Each report has different salary breakdowns and some district reports look less complete than other districts. If this is just 1 report at the local level in Tinley Park showing lack of uniformity, it's scary to think how bad the other reports are.

School Districts should be required to file and provide to the public, standard/uniform reports and documentation with data required by the ISBE each year. The lack of uniformity in the publicly provided ISBE salary and teacher count reports in just Tinley Park School Districts alone are evidence of a much needed reform in school reporting procedures. Just as taxpayers and businesses file standardized reports with the IRS and State, the ISBE should also require uniformity in reporting. This would allow for quicker and more efficient review and AUDITING.

Uniform reports must be required to provide taxpayers additional details...

You may notice (as we did) that School District reports of admin/teacher salaries are not uniform, making a simple audit much more difficult. This problem should be addressed by the School Districts and ISBE. Believe it or not, the information below is not required.

What should be listed on every School District report of teacher and administrator salaries and employee count (for auditing):

Also, to properly audit, we believe it is also important for taxpayers to know the TOTAL STAFF count within each district - including support staff, maintenance staff, etc. Currently, no local school district provides this information.

What should be listed on every School District report of teacher and administrator salaries and employee count (for auditing):

- Full Name

- Position (teacher/administrator)

- Department or Role (i.e. Math)

- Full Time or Part Time Status

- Years of Service

- Base Salary

- Health Insurance

- Extracurricular Activity Pay

- Pension/Retirement

- Bonuses

- Housing

- Vehicle Allowance

- Clothing Allowance

- Other (describe in report)

- Column Totals

- Total District Administrator & Teacher Count

Also, to properly audit, we believe it is also important for taxpayers to know the TOTAL STAFF count within each district - including support staff, maintenance staff, etc. Currently, no local school district provides this information.

Who monitors and verifies the accuracy of the reports that school boards submit to the ISBE?"

Student enrollment vs. staff counts

If taxpayers know the actual number of teachers and administrators at each school (see discrepancies above), it may be easier to determine if a district is over-staffed (in any department or role) based on school enrollment...

Elementary enrollmentDistrict 140: 3,623 enrolled students

Employees: Pending District 145: 1,454 enrolled students Employees: Pending District 146: 2,416 enrolled students Employees: Pending District 159: 1,947 enrolled students Employees: Pending District 161: 3,283 enrolled students Employees: Pending |

High School enrollment

District 210: 7,126 enrolled students

Employees: 567 1 staff per 12.6 students District 227: 3,303 enrolled students Employees: 665 1 staff per 5 students District 228: 5,196 enrolled students Employees: 549 1 staff per 9.5 students District 230: 7,786 enrolled students Employees: 829 1 staff per 9.4 students |

With enrollment down (and trending down) at area schools, how do schools justify such large staff counts?"

Illinois Standardized PARCC Exam Scores

In 2015 Illinois students took the new Partnership for Assessment of Readiness for College and Careers (PARCC) exam... see how your school district did: CLICK HERE

Administrator Benefits and Pensions

None of the Tinley Park School Districts provided Administrator Contracts with their public financial documents, but we located the documents through the government transparency advocate, Better Government Association. Each School District Administrator Contract is provided below for Taxpayers to review.

Elementary School Administrators |

High School Administrators |

|

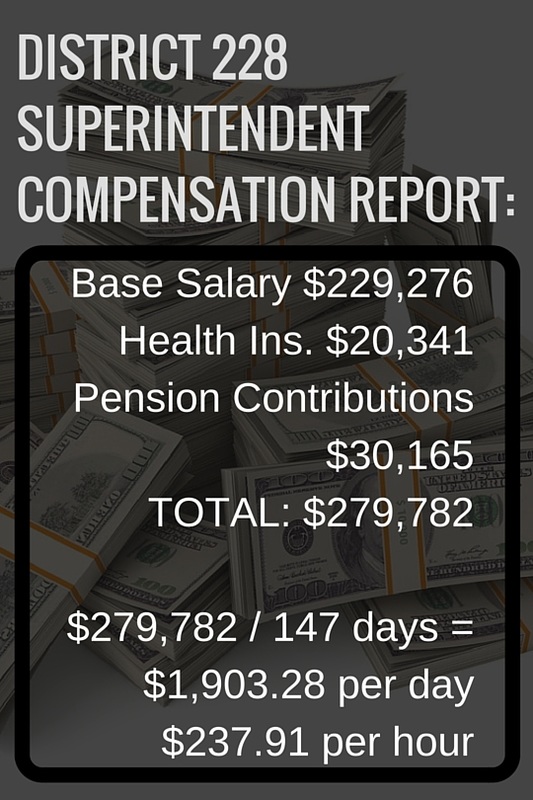

Without detailing the benefits and pensions from each Tinley Park school district and their slightly varying Administrators' contracts, here are details from Bremen High School District 228 Administrator contracts...

District 228 Administrator contracts span 5 years, with 4% annual pay increases. District Administrators are contracted to work 184 days per year. They receive all paid holidays that are observed by the school district, and also receive 20 days (4 weeks) of vacation time, PLUS they also receive 15 days (3 weeks) of sick leave and 2 days of personal leave where they receive full-pay... so contractually, Administrators only have to work 147 days per year. This equates to 218 days that Administrators don't work (60% of the year not working!) - which is LESS THAN A PART-TIME JOB! By contract, Administrators may also undertake outside [paid] consultation work, speaking engagements, writing, teaching a college/university course, lecturing or other professional duties - providing that this "other work" does not interfere with Administrator job duties. If an Administrator has employment terminated due to misconduct or other "for cause" reason, the board (taxpayers) pay Administrator salary and benefits until a legal/board review is completed. If employment is terminated at no fault, an Administrator receives the balance of salary owed for the remainder of the contract term, or $50,000 severance pay - whichever is less. |

|

District Administrators contribute NOTHING towards their TRS pension, instead, taxpayers are paying the Administrators 9.4% contribution as a "pick-up" (benefit). Administrators also contribute NOTHING towards their family health insurance plan, hospitalization or family dental plan - the taxpayers pay this expense in full. Besides their no-cost, full coverage health and dental plans, Administrators also receive a $750 yearly reimbursement towards an annual physical. District Administrators are covered by a $40,000 life insurance policy and are also covered by term life insurance at 2X their salary, both life insurance plans covered in full by taxpayers. Regular work-related automobile travel is reimbursed at at the IRS mileage rate [which is $0.54 per mile in 2016] and Administrators also receive reimbursed travel expenses. Administrators receive 100% tuition reimbursement towards one graduate course per semester if receiving an "A" grade, or 80% course reimbursement if receiving a "B" grade.

The District 228 Administrator's contract can be seen HERE.

According to the Teachers Retirement System (TRS), an Administrator's pension is calculated at 75% of the last 4 years of an administrator's highest average salary, and an annual 3% cost of living increase (compounded) is guaranteed. Administrators contribute NOTHING from their earnings to the TRS pension system, instead the district (taxpayers) pay this as an extra "perk"! The Administrator's pension is for LIFE, as is an annual 3% cost of living pension increase.

In 2005 Illinois enacted a law limiting end-of-career salary increases to 6%. Any increase above 6% incurs a penalty, which is charged to the school district (taxpayer). This has not stopped districts from giving large raises to teachers and administrators during the years that count towards calculating a lifetime pension. As seen in Homewood-Flossmoor's district 233, a superintendent received 20% salary increases in multiple years leading up to retirement. The state fined the district $225,884. The taxpayers are not only liable to pay that fine, but are liable for the illegally obtained 20% raises and increased lifetime pension payouts. This superintendent, who retired at age 57 in 2008, has already collected 1.68 million in pension and is expected to collect 10 million in lifetime pension payouts.

There are 3 fundamental problems with this current "6% salary law". 1) The raise cap of 6% should be lowered to the rate of inflation (which has been about 1%) a year. 2) Penalties should be imposed upon the individual receiving the raise. 3) The raise should be considered illegal and therefore void from salary and inclusion in pension calculations. Here is a recent Chicago Tribune article highlighting this problem: Click here to view.

The District 228 Administrator's contract can be seen HERE.

According to the Teachers Retirement System (TRS), an Administrator's pension is calculated at 75% of the last 4 years of an administrator's highest average salary, and an annual 3% cost of living increase (compounded) is guaranteed. Administrators contribute NOTHING from their earnings to the TRS pension system, instead the district (taxpayers) pay this as an extra "perk"! The Administrator's pension is for LIFE, as is an annual 3% cost of living pension increase.

In 2005 Illinois enacted a law limiting end-of-career salary increases to 6%. Any increase above 6% incurs a penalty, which is charged to the school district (taxpayer). This has not stopped districts from giving large raises to teachers and administrators during the years that count towards calculating a lifetime pension. As seen in Homewood-Flossmoor's district 233, a superintendent received 20% salary increases in multiple years leading up to retirement. The state fined the district $225,884. The taxpayers are not only liable to pay that fine, but are liable for the illegally obtained 20% raises and increased lifetime pension payouts. This superintendent, who retired at age 57 in 2008, has already collected 1.68 million in pension and is expected to collect 10 million in lifetime pension payouts.

There are 3 fundamental problems with this current "6% salary law". 1) The raise cap of 6% should be lowered to the rate of inflation (which has been about 1%) a year. 2) Penalties should be imposed upon the individual receiving the raise. 3) The raise should be considered illegal and therefore void from salary and inclusion in pension calculations. Here is a recent Chicago Tribune article highlighting this problem: Click here to view.

$5.95 Million in Penalties Imposed on TAXPAYERS

As explained in the section above, a 2005 Illinois law was intended to curtail big salary spikes and impose cash penalties on districts that give raises larger than 6 percent to retiring educators.

Tinley Park school districts have been violating the 6% limit and have inflicted [as of July 2015] nearly $6 MILLION in penalties upon taxpaying residents. Here are the numbers:

Tinley Park school districts have been violating the 6% limit and have inflicted [as of July 2015] nearly $6 MILLION in penalties upon taxpaying residents. Here are the numbers:

|

Elementary School District Penalties:

High School District Penalties:

TOTAL PENALTIES IMPOSED UPON TAXPAYERS: $5,950,041.71 |

|

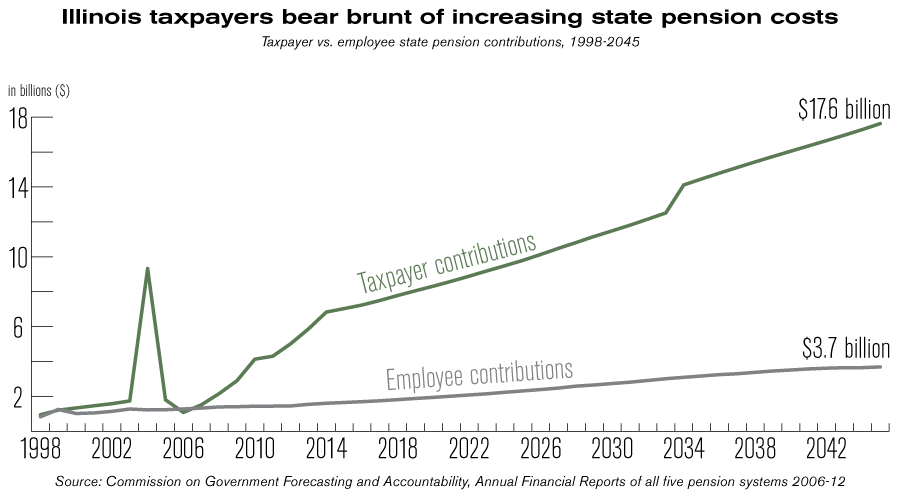

Teacher Benefits and Pensions

Each Tinley Park School District Teacher Contract is provided below for Taxpayers to review. Contracts are also posted to each school district website, which is provided on our "sources" page.

Elementary Teachers Contracts |

High School Teachers Contracts |

Without detailing the benefits and pensions from each Tinley Park school district and their slightly varying teachers union contracts, here are some details from the contracts of elementary school district 146 and Bremen high school district 228...

District 146 has teachers contracted to work 181 days per year at no more than 7 hours 30 minutes a day. Teachers also receive 15 days (3 weeks) of sick-leave where they receive full-pay, so teachers actually work only 166 days per year. This equates to 199 days that teachers don't work (55% of the year not working!). Teachers receive 100% reimbursement of their 1st masters degree and 50% of their second masters degree. Of course an advanced degree grants them an immediate pay increase as well. Teachers contribute 5% to their individual health care plan, and those with families contribute 25%. They receive $20,000 in life insurance and also get dental insurance paid for by the district (taxpayer). What a generous amount of benefits that NO taxpayer in the private sector has... yet we are paying these bills? The District 146 teacher's contract can be seen HERE.

District 228 has teachers contracted to work 181 days per year at no more than 7 hours 30 minutes a day. Instruction time is limited to 275 minutes (4.58 hours) and teachers are asked to be in class 15 minutes before their first class and stay until 15 minutes after their last class. Teachers receive 15 days (3 weeks) of sick-leave where they receive full-pay, so teachers actually work only 166 days per year. This equates to 199 days that teachers don't work (55% of the year not working!). Teachers contribute a flat 18% towards their health insurance plan, whether individual or an expensive family plan. They are covered by a $40,000 life insurance policy and dental insurance, paid in full by the district (taxpayer), and can also receive a $20,000 bonus to retire! The District 228 teacher's contract can be seen HERE.

Teacher contracts appear to all span 4-5 years, with 2.5%-6% annual pay increases, not including "lane", "step" or "scale" increases with taxpayer reimbursed degrees they receive.

A teacher's pension is calculated at 75% of the last 4 years of a teacher's highest average salary, and an annual 3% cost of living increase (compounded) is guaranteed. According to TRS, Teachers contribute 9.4% of their earnings to the TRS pension system, but some districts (taxpayers) pay this as an extra "perk"! If a teacher is contributing 9.4% to their pension, it is only 1.75% more than the 7.65% us taxpayers are required to pay into Social Security... taxpayers, however, not receiving anything remotely close to a TRS pension from Social Security. The teachers' pension is for LIFE, as is an annual 3% cost of living pension increase, AND their generous health insurance coverage is paid by taxpayers for life. At the rates Tinley Park administrators and teachers are paid, taxpayers are on the hook for million dollar pensions PER administrator and teacher. This is unsustainable.

It's no wonder even as property values decrease, property taxes continue to increase...

District 146 has teachers contracted to work 181 days per year at no more than 7 hours 30 minutes a day. Teachers also receive 15 days (3 weeks) of sick-leave where they receive full-pay, so teachers actually work only 166 days per year. This equates to 199 days that teachers don't work (55% of the year not working!). Teachers receive 100% reimbursement of their 1st masters degree and 50% of their second masters degree. Of course an advanced degree grants them an immediate pay increase as well. Teachers contribute 5% to their individual health care plan, and those with families contribute 25%. They receive $20,000 in life insurance and also get dental insurance paid for by the district (taxpayer). What a generous amount of benefits that NO taxpayer in the private sector has... yet we are paying these bills? The District 146 teacher's contract can be seen HERE.

District 228 has teachers contracted to work 181 days per year at no more than 7 hours 30 minutes a day. Instruction time is limited to 275 minutes (4.58 hours) and teachers are asked to be in class 15 minutes before their first class and stay until 15 minutes after their last class. Teachers receive 15 days (3 weeks) of sick-leave where they receive full-pay, so teachers actually work only 166 days per year. This equates to 199 days that teachers don't work (55% of the year not working!). Teachers contribute a flat 18% towards their health insurance plan, whether individual or an expensive family plan. They are covered by a $40,000 life insurance policy and dental insurance, paid in full by the district (taxpayer), and can also receive a $20,000 bonus to retire! The District 228 teacher's contract can be seen HERE.

Teacher contracts appear to all span 4-5 years, with 2.5%-6% annual pay increases, not including "lane", "step" or "scale" increases with taxpayer reimbursed degrees they receive.

A teacher's pension is calculated at 75% of the last 4 years of a teacher's highest average salary, and an annual 3% cost of living increase (compounded) is guaranteed. According to TRS, Teachers contribute 9.4% of their earnings to the TRS pension system, but some districts (taxpayers) pay this as an extra "perk"! If a teacher is contributing 9.4% to their pension, it is only 1.75% more than the 7.65% us taxpayers are required to pay into Social Security... taxpayers, however, not receiving anything remotely close to a TRS pension from Social Security. The teachers' pension is for LIFE, as is an annual 3% cost of living pension increase, AND their generous health insurance coverage is paid by taxpayers for life. At the rates Tinley Park administrators and teachers are paid, taxpayers are on the hook for million dollar pensions PER administrator and teacher. This is unsustainable.

It's no wonder even as property values decrease, property taxes continue to increase...

There is currently a music teacher collecting $135,000 in compensation and a village planning director collecting $165,000 in compensation on the same Tinley Park elementary district school board. (The village planning director recently resigned after serious misconduct allegations, but remains on the Tinley Park School District 146 School Board). This is a board of people approving school salaries, contracts and spending. Isn't it a conflict of interest and perpetuating a cycle of financial delusion by having school and village employees on a school board managing taxpayer money? Especially when there is a board member that resigned from their job and is named as a defendant in a lawsuit over alleged illegal activity?

Taxpayers are being forced to pay lifetime salaries to every civil servant, teacher, state worker and politician. After paying out "pension salaries" and benefits to the retired, we then have to hire more civil servants, teachers, state workers and politicians. There isn't enough money going into the system to support paying out lifetime salaries and benefits to each state, municipal and school employee. It's a vicious, unsustainable cycle. Perhaps this is why the private sector utilizes 401k and other sustainable retirement plans! Taxpayers aren't given 2.5-6% annual raises, our houses do not appreciate 2.5-6% per year and we don't receive a guaranteed pension for life as retirement. The public system of pay/benefits needs to be restructured to the proven system in which the private sector utilizes.

Taxpayers can't afford to be on the hook for bad math and intentional under-funding. Taxpayers are not the guarantors of pensions.

Only six states have paid a lower percentage of their annual pension payments than Illinois since 2001, according to a recent report from the National Association of State Retirement Administrators.

Every municipality and school district in our State bought into a costly and unsustainable system. The only way out may be municipal and school district bankruptcy, which HAS been done. The system needs to be restructured.

Taxpayers are being forced to pay lifetime salaries to every civil servant, teacher, state worker and politician. After paying out "pension salaries" and benefits to the retired, we then have to hire more civil servants, teachers, state workers and politicians. There isn't enough money going into the system to support paying out lifetime salaries and benefits to each state, municipal and school employee. It's a vicious, unsustainable cycle. Perhaps this is why the private sector utilizes 401k and other sustainable retirement plans! Taxpayers aren't given 2.5-6% annual raises, our houses do not appreciate 2.5-6% per year and we don't receive a guaranteed pension for life as retirement. The public system of pay/benefits needs to be restructured to the proven system in which the private sector utilizes.

Taxpayers can't afford to be on the hook for bad math and intentional under-funding. Taxpayers are not the guarantors of pensions.

Only six states have paid a lower percentage of their annual pension payments than Illinois since 2001, according to a recent report from the National Association of State Retirement Administrators.

Every municipality and school district in our State bought into a costly and unsustainable system. The only way out may be municipal and school district bankruptcy, which HAS been done. The system needs to be restructured.

School District Pension Liabilities

Interesting Findings

- District 159 operates on a budget that is over $26 MILLION more than District 145.

- District 140 reports a 7.08% pension fund ratio, making taxpayers in this District liable for nearly 93% of the pension fund debt.

- District 210 and 228 rank among the highest deficit spenders in Illinois. Click Here to read an article highlighting this issue and read below for additional details. District 227 and 140 are not far behind in deficit spending.

- Annual salary increases in ALL local school districts exceed the annual rate of inflation. District 145 and 228 is at the highest annual salary rate increase of 5.75%, and no school district is below a 3.75% annual salary increase per yer.

- The health care cost "trend" in ALL local school districts is between 7.5-8%, requiring a higher tax levy every year.

- District 159 and District 227 are NOT REQUIRED to report unfunded OPEB (other post-employment benefits - i.e. health ins), which skews their actual unfunded liability numbers.

- Local School Districts annually increase their tax levy even though all but one district (210) carries large surpluses in their reserves. It's concerning that schools are retaining so much TAXPAYER dollars in their accounts as a reserve.

- Based on student enrollment, the reported FTE staff count (per the Cook County Treasurer Reports, provided below) and ISBE report of Teacher/Admin count (provided below) shows that schools may be over-staffed, costing taxpayers unnecessary salaries and benefits of personnel. There are large staff discrepancies between the School Districts. More in-depth reporting by school districts is necessary to properly analyze, and currently, this type of reporting is not required by the State.

Elementary SchoolsDistrict 140

Pension/OPEB Funded Ratio: 7.08% (see page 7-8 below) Operating Budget 2016: $53,901,500 Year-End 2015 Fund Balance: $51,983,041 (see page 26) Total Agency Employees or Full-Time Equivalents (FTE): 537 District FTE count per Pupil: 6.75 ISBE Report Count of Teachers/Admin: 271 IBSE count per Pupil: 13.37 Difference between FTE and ISBE count: 266 Annual Rate of Salary Increases: 3.00% Health Care Cost Trend Rate: 8.00% 3,623 enrolled students District 145 Pension/OPEB Funded Ratio: 74.37% (see page 9-10 below) Operating Budget 2015: $16,256,691 Year-End 2016 Fund Balance: $6,342,015 (see page 19) Total Agency Employees or Full-Time Equivalents (FTE): 216 District FTE count per Pupil: 6.73 ISBE Report Count of Teachers/Admin: 97 IBSE count per Pupil: 14.99 Difference between FTE and ISBE count: 119 Annual Rate of Salary Increases: 5.75% Health Care Cost Trend Rate: 7.50% 1,454 enrolled students District 146 Pension/OPEB Funded Ratio: 90.98% (see page 11-12 below) Operating Budget 2015: $38,458,921 Year-End 2015 Fund Balance: $33,446,715 (see page 38) Total Agency Employees or Full-Time Equivalents (FTE): 393 District FTE count per Pupil: 6.15 ISBE Report Count of Teachers/Admin: 242 IBSE count per Pupil: 9.98 Difference between FTE and ISBE count: 151 Annual Rate of Salary Increases: 3.75% Health Care Cost Trend Rate: 8.00% 2,416 enrolled students District 159 Pension Funded Ratio: 91.21% - This District is NOT required to report any OPEB (Other Post-Employment Benefits) in its Financial Statements. The ratio reported is not including unfunded benefits. (see page 13-14 below) Operating Budget 2015: $42,710,019 Year-End 2016 Fund Balance: $18,027,291 (see page 19) Total Agency Employees or Full-Time Equivalents (FTE): 298 District FTE count per Pupil: 6.53 ISBE Report Count of Teachers/Admin: 319 IBSE count per Pupil: 6.10 Difference between FTE and ISBE count: 74 Annual Rate of Salary Increases: 4.00% Health Care Cost Trend Rate: Not required to report 1,947 enrolled students District 161 Research pending on this Will County district. Year-End 2016 Fund Balance: $15,632,229 (see page 20) 3,283 enrolled students |

High SchoolsDistrict 210

Pension/OPEB Funded Ratio: 85.02% (see page 15-16 below) Operating Budget 2015: $114,165,116 Year-End 2016 Fund Balance: $1,886,696 (see page 20) Total Agency Employees or Full-Time Equivalents (FTE): 842 District FTE count per Pupil: 8.46 ISBE Report Count of Teachers/Admin: 463 IBSE count per Pupil: 15.39 Difference between FTE and ISBE count: 379 Annual Rate of Salary Increases: 3.00% Health Care Cost Trend Rate: 8.00% 7,126 enrolled students District 227 Pension Funded Ratio: 93.17% - This District is NOT required to report any OPEB (Other Post-Employment Benefits) in its Financial Statements. The ratio reported is not including unfunded benefits. (see page 17-18 below) Operating Budget 2015: $58,203,831 Year-End 2016 Fund Balance: $30,089,209 (see page 18) Total Agency Employees or Full-Time Equivalents (FTE): 576 District FTE count per Pupil: 5.73 ISBE Report Count of Teachers/Admin: 255 IBSE count per Pupil: 12.95 Difference between FTE and ISBE count: 321 Annual Rate of Salary Increases: 4.00% Health Care Cost Trend Rate: Not required to report 3,303 enrolled students District 228 Pension/OPEB Funded Ratio: 88.35% (see page 19-20 below) Operating Budget 2015: $86,609,537 Year-End 2016 Fund Balance: $47,140,213 (see page 19) Total Agency Employees or Full-Time Equivalents (FTE): 583 District FTE count per Pupil: 8.91 ISBE Report Count of Teachers/Admin: 338 IBSE count per Pupil: 15.37 Difference between FTE and ISBE count: 245 Annual Rate of Salary Increases: 5.75% Health Care Cost Trend Rate: 7.50% 5,196 enrolled students District 230 Pension/OPEB Funded Ratio: 75.93% (see page 21-22 below) Operating Budget 2015: $123,806,276 Year-End 2016 Fund Balance: $60,843,567 (see page 20) Total Agency Employees or Full-Time Equivalents (FTE): 836 District FTE count per Pupil: 9.31 ISBE Report Count of Teachers/Admin: 567 IBSE count per Pupil: 13.73 Difference between FTE and ISBE count: 269 Annual Rate of Salary Increases: 3.75% Health Care Cost Trend Rate: 7.50% 7,786 enrolled students |

School Deficit Spending in 2016

|

Related Articles |

|

In fiscal year 2016, the following Tinley Park School Districts ranked among the highest in school district deficit spending in Illinois:

|

|

What does all of this data mean?

There is no possibility of our property taxes, or Illinois taxes to be reduced based on the annually increasing costs of School District (and Village) salary/benefit costs. Our School Districts and Village also carry unfunded liabilities, and in some cases large unfunded liabilities, which are leaving taxpayers on the hook for increased tax levies to bring these funds to acceptable levels. Taxpayers are also liable for the bonds that the Schools and Village receive, and all of the financial risks that the Schools and Village expose taxpayers to. The way of Municipal and State management needs to be restructured into a fiscally responsible business model with: less government bloat, realistic salaries and benefits, standardized reporting for in-depth auditing/analysis, more transparency and better oversight. The local government's way of the past, and especially the School District and Village spending boom between 2000-2015+ set us on a terrible course with no way to truly recover unless spending is reduced and costs are capped - making tax burdens a much smaller and more manageable percentage of taxpayer income (and also more in line with neighboring States).

One way to reduce tax burdens is to consolidate school districts, which not only will undoubtedly lower tax burdens and also create a more efficient system.

One way to reduce tax burdens is to consolidate school districts, which not only will undoubtedly lower tax burdens and also create a more efficient system.

Pensions vs. Social Security

The discrepancy between administrator/teacher pensions and social security benefits that taxpayers receive is astounding. How is the average social security benefit $1,230 per month when the average teacher pension is $6,058 per month with each person investing virtually the same percentage per paycheck? And why is the earliest age to receive social security benefits 67 years old when a teacher can retire at age 55*?

Based on social security benefits, a retired homeowner in Tinley Park receiving the average social security $1,230 monthly check will spend virtually 35% of their retirement income on just a property tax bill of $5,000. A homeowner that has invested in a home, paid off a mortgage, and kept up a home in this community is essentially being evicted by the village through property taxes. Suburban teacher pensions are breaking the taxpayers' banks.

Homeowners will not be held hostage and we will not be without a voice when it comes to property taxes.

*Public Act 96-0889 added a new section to the Pension Code that applies different benefits to anyone who first contributes to TRS on or after Jan. 1, 2011 and does not have any previous service credit with a pension system that has reciprocal rights with TRS. These members are referred to as “Tier II” members where pension changes include: raising minimum eligibility to draw a retirement benefit to age 67 (to receive full benefits) with 10 years of service, initiating a cap on the salaries used to calculate retirement benefits, and limiting cost-of-living annuity adjustments to the lesser of 3 percent or ½ of the annual increase in the Consumer Price Index, not compounded. The retirement formula is unchanged. The new pension law does not apply to anyone who has TRS service prior to Jan. 1, 2011.

Based on social security benefits, a retired homeowner in Tinley Park receiving the average social security $1,230 monthly check will spend virtually 35% of their retirement income on just a property tax bill of $5,000. A homeowner that has invested in a home, paid off a mortgage, and kept up a home in this community is essentially being evicted by the village through property taxes. Suburban teacher pensions are breaking the taxpayers' banks.

Homeowners will not be held hostage and we will not be without a voice when it comes to property taxes.

*Public Act 96-0889 added a new section to the Pension Code that applies different benefits to anyone who first contributes to TRS on or after Jan. 1, 2011 and does not have any previous service credit with a pension system that has reciprocal rights with TRS. These members are referred to as “Tier II” members where pension changes include: raising minimum eligibility to draw a retirement benefit to age 67 (to receive full benefits) with 10 years of service, initiating a cap on the salaries used to calculate retirement benefits, and limiting cost-of-living annuity adjustments to the lesser of 3 percent or ½ of the annual increase in the Consumer Price Index, not compounded. The retirement formula is unchanged. The new pension law does not apply to anyone who has TRS service prior to Jan. 1, 2011.

Mapping the $100,000+ Illinois Teacher Pensions Costing Taxpayers Nearly $1.0 BillionForbes contributor Adam Andrzejewski writes:

New numbers show that the 7,499 ‘highly compensated,’ six-figure school administrator/teacher retirees cost IL taxpayers nearly $1 billion per year. But in just six years, the problem of six-figure pensions will be three-times worse. In 2014 I wrote in Forbes about a pair of union lobbyists who substitute taught for one-day in the public schools and then started collecting over $1 million of lifetime public ‘teacher’ pension payout – despite a state law expressly designed to stop them... This week, our organization at OpenTheBooks.com debuted our interactive info mapping platform giving context to the 7,499 retired Illinois educators who pulled-down a pension of $100,000 or more. These retirees cost Illinois taxpayers $900 million (2015). Individually, these pension millionaires contributed so little to the system that they ‘broke-even’ on their ‘cost-basis’ within the first 20-months of retirement. Read the entire Forbes article HERE. |

There are MANY administrators, teachers and public employees collecting $100,000 pensions per year in retirement, as highlighted by this interactive graph (click the photo above to view). You may be shocked at how many people are even collecting $15-20,000 PER MONTH in taxpayer funded pensions! This is a must see.

|

Top 5 highest paid teachers in each district

(excluding administrators and Principals, who generally are highest paid)

Based on board provided ISBE reports. Average includes administration, teachers, and part-time teacher base salaries, bonuses and benefits.

|

District 140:

(5th grade) $118,310* (3rd grade) $112,997* (special services) $112,831* (band director) $109,757* (6th grade) $109,554* Average district salary: $76,769* *Includes base salary plus all listed bonuses and benefits District 145: (LD resource) $109,260* (social worker) $101,015* (social studies, 8) $97,448* (3rd grade) $81,353* (2nd grade) $79,869* Average district salary: $61,384* *Includes base salary plus all listed bonuses and benefits District 146: (3rd grade) $125,997* (3rd grade) $121,802* (music) $120,598* (reading) $117,040* (language arts) $115,644* (1st grade) $114,410* Average district salary: $75,023* *Includes base salary plus all listed bonuses and benefits District 159: (3rd grade) $102,817 (kindergarten) $102,817 (english) $102,120 (2nd grade) $99,434 (music) $96,820 Average district salary: 59,883* *Report is not complete, benefit totals not provided District 161: (2nd grade) $118,252* (6th grade) $108,610* (1st grade) $104,534* (reading) $103,548* (band) $101,180* Average district salary: $67,417* *Includes base salary plus all listed bonuses and benefits |

District 210:

(physical ed) $181,028* (physical ed) $148,325* (english) $141,760* (art) $141,759* (science) $141,759* Average district salary: $85,974* *Includes base salary plus all listed bonuses and benefits District 227: (physical ed) $156,475* (math) $155,855* (untitled) $122,486* (world language) $121,056* (social studies) $120,693* Average district salary: $80,170* *Includes base salary plus all listed bonuses and benefits District 228: (arts) $215,704* (arts) $173,196* (math) $172,418* (math) $172,272* (social science) $168,311* (social science) $163,798* Average district salary: $117,023* *Includes base salary plus all listed bonuses and benefits District 230: (english) $147,244* (social studies) $147,235* (untitled) $147,234* (english) $147,234* (special services) $147,226* Average district salary: $99,814* *Includes base salary plus all listed bonuses and benefits |

Keep in mind, here are the Highest paid occupations as reported by Forbes and the BLS:

Districts are nontransparent on not-for-profits

As detailed in a Chicago Sun-Times Article on 8/6/16, Reporter Chris Fusco writes:

"The not-for-profit association that oversees high school sports in Illinois can continue to keep details about its contracts, sponsorships and other financial matters secret under a court ruling that comes in the wake of it reporting a six-figure increase in payouts related to retirees. The Illinois High School Association (IHSA) paid $888,425 out of its two retirement funds in the 2014-15 school year, according to financial statements it filed with the Illinois attorney general’s office. That’s up $259,876, or 41 percent, from the previous year. The organization’s contributions into its main pension plan and the second retirement plan went up by 48 percent over the previous year, to $592,710, the records show.

If the IHSA were a public agency, it would have to reveal the names of the retirees getting the money, how much they’re paid and who’s managing the organization’s retirement accounts. But a three-judge panel of the first district Illinois Appellate Court unanimously ruled in June that the IHSA isn’t a government body and thus isn’t subject to disclosure requirements under the Illinois Freedom of Information Act. That case has since been appealed to the Illinois Supreme Court, which hasn’t decided yet whether to hear it.

...The Better Government Association sued the association in 2014 after the Chicago Sun-Times reported its costs for salaries and benefits had gone up as revenues and profits from its marquee event, the state boys’ basketball tournament, declined. The BGA argued the IHSA should be treated like a government body because it “performs a governmental function” and generates income “from events involving predominantly public schools.”

But the appellate court ruled that “any school can decide to forego participation in the IHSA.” Justices also noted the association doesn’t get money directly from taxpayers, generating most of its income through revenue-sharing agreements on ticket sales at school playoff sporting events. Attorneys Matt Topic and Joshua Burday filed the watchdog group’s appeal to the state’s high court on July 29.

“This is an issue of significant public interest,” they wrote. “Government is increasingly privatizing a wide array of its functions. Without a broader and more sensible test for ‘governmental function,’ crucial government business could be privatized in a way that leaves the public in the dark and without the ability to hold anyone accountable.”

Click here to read the Sun-Times article in its entirety

"The not-for-profit association that oversees high school sports in Illinois can continue to keep details about its contracts, sponsorships and other financial matters secret under a court ruling that comes in the wake of it reporting a six-figure increase in payouts related to retirees. The Illinois High School Association (IHSA) paid $888,425 out of its two retirement funds in the 2014-15 school year, according to financial statements it filed with the Illinois attorney general’s office. That’s up $259,876, or 41 percent, from the previous year. The organization’s contributions into its main pension plan and the second retirement plan went up by 48 percent over the previous year, to $592,710, the records show.

If the IHSA were a public agency, it would have to reveal the names of the retirees getting the money, how much they’re paid and who’s managing the organization’s retirement accounts. But a three-judge panel of the first district Illinois Appellate Court unanimously ruled in June that the IHSA isn’t a government body and thus isn’t subject to disclosure requirements under the Illinois Freedom of Information Act. That case has since been appealed to the Illinois Supreme Court, which hasn’t decided yet whether to hear it.

...The Better Government Association sued the association in 2014 after the Chicago Sun-Times reported its costs for salaries and benefits had gone up as revenues and profits from its marquee event, the state boys’ basketball tournament, declined. The BGA argued the IHSA should be treated like a government body because it “performs a governmental function” and generates income “from events involving predominantly public schools.”

But the appellate court ruled that “any school can decide to forego participation in the IHSA.” Justices also noted the association doesn’t get money directly from taxpayers, generating most of its income through revenue-sharing agreements on ticket sales at school playoff sporting events. Attorneys Matt Topic and Joshua Burday filed the watchdog group’s appeal to the state’s high court on July 29.

“This is an issue of significant public interest,” they wrote. “Government is increasingly privatizing a wide array of its functions. Without a broader and more sensible test for ‘governmental function,’ crucial government business could be privatized in a way that leaves the public in the dark and without the ability to hold anyone accountable.”

Click here to read the Sun-Times article in its entirety

Evidence of District 230 evading FOIA? What are they hiding?

Check out the FOIA request the BGA (Better Government Association) made with School District 230, and read District 230's response. This lead to the BGA suing District 230 and the IHSA for a rather simple request for information.

FOIA may not apply to IHSA according to the above court ruling... but it does apply to School Districts

Taxpayers must start asking about the fees paid by out to (and received by) "not-for-profit organizations" by our school districts. Reviewing the sheer number of organizations marketed to school administrators and employees has us concerned about the sheer amount of TAXPAYER DOLLARS being funneled to these organizations (and their lobbyists)... and how these non-profit organizations are closely interlaced with our school districts, yet not legally responsible to taxpayers. Furthermore, citizens elect school boards to represent the citizens, so it is concerning to find "non-profit" organizations providing school boards information and data which the citizens are not privy to. The information many "organizations" provide our publicly funded school system employees appear more like collusion, or at the minimum, conflict of interest - especially when organizations discuss (indoctrinate) public policy and politics. Read the "join" page of some of the organizations to see what they provide their members. These organizations appear to be more like additional, privatized unions.

Lobbyists within these "organizations" and "not-for-profits" are being paid with taxpayers dollars, and in many instances these lobbyists are working AGAINST taxpayers.

We found "not-for-profits" marketed to school principals, school deans, school superintendents, school boards, school attorneys, school sports programs, and more... all at state and national levels that most of the school districts pay for (on behalf of the school/employee) with TAXPAYER dollars. Many of these "not-for-profit" organizations also provide professional liability insurance, so technically we are paying to insure school district employees against ourselves if we have a claim against them for wrong-doing! Some of these "non-profit organizations" even appear to be privatizing certain roles and functions of our districts that do not have to adhere to FOIA or other taxpayer protection laws based on their organizational structure.

Taxpayers must know how much in "dues and fees" school districts pay "not-for-profits" and their lobbyists with taxpayer dollars... not to mention the reimbursed travel expenses taxpayers cover when school administrators/employees go to conferences sponsored by these "non-profits". Taxpayers must also know who the lobbyists are in each organization and what their role is within the organization, what they lobby for, what they are paid, etc.

Lobbyists within these "organizations" and "not-for-profits" are being paid with taxpayers dollars, and in many instances these lobbyists are working AGAINST taxpayers.

We found "not-for-profits" marketed to school principals, school deans, school superintendents, school boards, school attorneys, school sports programs, and more... all at state and national levels that most of the school districts pay for (on behalf of the school/employee) with TAXPAYER dollars. Many of these "not-for-profit" organizations also provide professional liability insurance, so technically we are paying to insure school district employees against ourselves if we have a claim against them for wrong-doing! Some of these "non-profit organizations" even appear to be privatizing certain roles and functions of our districts that do not have to adhere to FOIA or other taxpayer protection laws based on their organizational structure.

Taxpayers must know how much in "dues and fees" school districts pay "not-for-profits" and their lobbyists with taxpayer dollars... not to mention the reimbursed travel expenses taxpayers cover when school administrators/employees go to conferences sponsored by these "non-profits". Taxpayers must also know who the lobbyists are in each organization and what their role is within the organization, what they lobby for, what they are paid, etc.

Here is a quick tip on what you, the taxpayer, can FOIA your school district for... or even demand at a school board meeting. Bring your family, friends, neighbors and local business leaders in for support and to stand up and demand answers.

Request by FOIA (or at a public school board meeting):

*A help guide to bring to the board meeting has been made available to download here. |

|

Taxpayers must also know more about the law firms that represent our school district and the legal fees our school districts pay, all in order to give us insight to issues that may be occurring within our schools. An insider informed us that "some non-profit organizations charge money to our school districts for items such as case summaries in the amounts of $450 and $1,000 each, but provide access to case summaries for free if a School Districts becomes a member of their organization". These non-profits do not publicly state what the dues are for districts to become members. However, case law is public information that can be easily obtained on the Internet for free and it is information that a superintendent should be qualified to understand. The insider also told us that "school boards appear to be using only two select insurance organizations... If there is a monopoly on insurance carriers for workman's comp and professional liabilities for school districts then we may be incurring unnecessarily higher fees, paid with taxpayer funds."

Not-for-profits include but are not limited to:

Additional non-profit organizations include:

- IADA, Illinois Athletic Directors Association (www.ada.8to18.com)

- IATA, Illinois Athletic Trainers Associations (www.illinoisathletictrainers.org)

- IASA, Illinois Association of School Administrators (www.iasaedu.org)

- IASB, Illinois Association of School Boards (www.iasb.com)

- IASC, Illinois Association of Student Councils (www.illinoisstuco.org)

- IARSS, Illinois Association of Regional Superintendents of Schools (www.iarss.org)

- IBCA, Illinois Basketball Coaches Association (www.ibcaillinois.org)

- ICCA, Illinois Cheerleading Coaches Association (www.cheericca.org)

- ICSA, Illinois Council of School Attorneys (www.iasb.com/lawdir/exec.cfm)

- IDSA, Illinois Directors of Student Activities (www.idsa-activities.org)

- IESA, Illinois Elementary School Association (www.iesa.org)

- IHSA, Illinois High School Association, (www.ihsa.org)

- IHSFCA, Illinois High School Football Coaches Assoc. (www.ihsfca.com)

- IPA, Illinois Principals Association (www.ilprincipals.org)

- ISDA, Illinois State Deans Association (ISDA)

- See more school sports/activity organization links here

Additional non-profit organizations include:

- AAHPERD, American Alliance for Health, Physical Education, Recreation and Dance (www.aahperd.org)

- AASA, American Association of School Administrators (www.aasa.org)

- AASL, American Association of School Librarians (www.ala.org/aasl)

- ACEI, Association for Childhood Education International (www.acei.org)

- ACTFL, American Council on the Teaching of Foreign Languages (www.actfl.org)

- AECT, Association for Educational Communications and Technology (www.aect.org)

- AERA, American Educational Research Association (www.aera.org)

- AESA, Association of Educational Service Agencies (www.aesa.us)

- AFSA, American Federation of School Administrators (www.afsaadmin.org)

- AFT, American Federation of Teachers (www.aft.org)

- ALAS, Association of Latino Administrators and Superintendents (www.alasedu.net)

- AMLE, Association for Middle Level Education (www.amle.org)

- ASBO, Association of School Business Officers International (www.asbointl.org)

- ASCD, Learn, Teach, Lead (www.ascd.org)

- ASCA, American School Counselor Association (www.schoolcounselor.org)

- ASIS International, Advancing Security Worldwide (www.asisonline.org)

- CEC, Council for Exceptional Children (www.cec.sped.org)

- CEFPI, Council of Educational Facilities Planners International (www.cefpi.org)

- CoSN, Council for School Networking (www.cosn.org)

- FETC, Florida Educational Technology Conference, (www.fetc.org)

- InfoComm, Information Communications Marketplace (www.infocommshow.org)

- IRA, International Reading Association (www.reading.org)

- ISTE, International Society for Technology in Education (www.iste.org)

- NAEA, National Art Education Association (www.arteducators.org)

- NAESP, National Association of Elementary School Principals (www.naesp.org)

- NAEYC, National Association for the Education of Young Children (www.naeyc.org)

- NAfME, National Association for Music Education (www.nafme.org)

- NAGC, National Association for Gifted Children (www.nagc.org)

- NASBE, National Association of State Boards of Education (www.nasbe.org)

- NASSP, National Association of Secondary School Principals (www.nassp.org)

- NBEA, National Business Education Association (www.nbea.org)

- NCSS, National Council for the Social Studies (www.ncss.org)

- NCTE, National Council of Teachers of English (www.ncte.org)

- NCTM, National Council of Teachers of Mathematics (www.nctm.org)

- NEA, National Education Association (www.nea.org)

- NFHS, National Federation of State High School Assocations (www.nfhs.org)

- NSBA, National School Boards Association (www.nsba.org)

- NSTA, National Science Teachers Association (www.nsta.org)

- PTA, National Parent Teachers Association (www.pta.org)

- SETDA, State Educational Technology Directors Association (www.sedta.org)

- TCEA, Texas Computer Education Association (www.tcea.org)

- USDLA, United States Distance Learning Association (www.usdla.org)

School Contracts Shrouded in Secrecy

"Here’s how the process works now: School districts and teachers’ unions begin negotiating new contracts months before a previous contract expires. These negotiations are not open to the public. Once a tentative agreement has been reached, each side votes. The teachers vote to ratify the contract, and the school board votes to approve the contract. Sometimes school boards release snippets of information about the provisions contained in the contract. But most often, the full contract is not released to the public until after both sides have voted and the contract is a done deal – leaving the public no room to voice concerns during negotiations." - Mailee Smith, Illinois Policy Group

Illinois School Districts pass closed-door budgets, expect Taxpayers to fork over more money.

Compare Pensions by State

The "compare states" feature of the public sector pension calculator shows Illinois paying much higher pensions than other states with the exact same salary and years of service data used to determine pension rates. Per the Manhattan Institute Organization: "These are estimates, as of 2013. Pension benefits' exact value can be affected by numerous factors that vary between systems, such as "pension spiking" and cost-of-living-adjustment provisions."

If it's stuck, take your head out to see what's happening

|

In general, pure complacency has contributed to nothing [good] getting done in this State, our Village and School Districts for many years. They say the fish rots from the head down, so with corruption and greed rampant at the local level, as a State we're pretty much financially rotten. This is seen in "prevailing wage" rates of pay, unfunded pension liabilities in the Villages and Schools, massive and even unnecessary spending in budgets... just like in the State and the Government. Something needs to be done to address the Pension debt across the board, throughout every facet of government. Taxpayers need to shrink the massive industry of Government in Illinois.

|

The Great American Ponzi Scheme

Ponzi Scheme definition: "A Ponzi scheme is a fraudulent investment operation where the operator, an individual or organization, pays returns to its investors from new capital paid to the operators by new investors, rather than from profit earned through legitimate sources. Operators of Ponzi schemes usually entice new investors by offering higher returns than other investments, in the form of short-term returns that are either abnormally high or unusually consistent. Ponzi schemes occasionally begin as legitimate businesses, until the business fails to achieve the returns expected. The business becomes a Ponzi scheme if it then continues under fraudulent terms. Whatever the initial situation, the perpetuation of the high returns requires an ever-increasing flow of money from new investors to sustain the scheme." - United States Security & Exchange Commission

According to the Civic Federation, a budget watchdog, "Illinois has piled up a whopping $111 billion in unfunded pension liabilities, in addition to $56 billion in debt for health benefits for pensioners. The state devotes one in four of its tax dollars to pensions, which is more than it spends on primary and secondary education." Read more about that here. The argument is not about cutting funding for students, it's about cutting budgets where necessary and restructuring pensions and benefits - which receive more money than the State spends on primary and secondary education! When obligations outgrow the tax base there are MAJOR problems to address, and burying our heads in the sand will not make it go away.

No reasonable taxpayer would suggest that any public employee lose what they have personally contributed to their retirement, and that should never happen - just like it should never happen to taxpayers who have paid into the FEDERALLY REQUIRED ponzi scheme of social security and medicare their entire working lives. However, the idea of a lifetime "pension salary" for public employees is far fetched at this stage of State and community financial decay. It's fiscally impossible to cover all pension debts without collapsing every other system, industry and household in the State of Illinois. This State is in, what's considered by economists, a death spiral. Public pension and benefit systems need to be quickly amended and ultimately restructured into a fiscally responsible system - the same applies to social security too. Taxpayers know the feeling of retirement planning adjustments. Many taxpayers have been left with major losses after the economic collapse in 2008, and the collapse is still continuing now.

Obviously, the problem with pensions are all rooted in money - public employees are fighting to keep their generous pay and benefits and taxpayers are fighting to keep their taxes down and afford their bills. There is a common ground that can be reached, but it's up to public employees to work together and for the taxpaying citizens. Most taxpayers would not argue with public employees making an income consistent with local costs of living, contributing private sector rates to their health plan and contributing private sector rates to a defined contribution 401k-type retirement account. If this type of idea keeps getting fought by public employees, taxpayers' livelihoods will continue to be at stake as the tax burdens continue to fall solely on TAXPAYERS. This is where the hostility arises in these arguments. Most taxpayers savings, retirement accounts and lifestyles have all been diminished to afford the increasing cost of living and continually rising property taxes. Asking more from the taxpayers who are beyond financially extended to cover excessive costs of public salaries and benefits will never be met with acceptance. We understand the State did not contribute enough to the pension system, but the pension system ponzi scheme was never sustainable to begin with - its a ponzi scheme. It all looks good on paper, everyone involved in the pension ponzi knew what they wanted from it, but it was never sustainable. Public employees can blame the State, but Taxpayers blame all parties involved for agreeing to it, letting it continue, and causing it to directly affect us.

The fate of this State is going to come down greed or reason. We like to believe that public employees can reason on an acceptable resolution.

According to the Civic Federation, a budget watchdog, "Illinois has piled up a whopping $111 billion in unfunded pension liabilities, in addition to $56 billion in debt for health benefits for pensioners. The state devotes one in four of its tax dollars to pensions, which is more than it spends on primary and secondary education." Read more about that here. The argument is not about cutting funding for students, it's about cutting budgets where necessary and restructuring pensions and benefits - which receive more money than the State spends on primary and secondary education! When obligations outgrow the tax base there are MAJOR problems to address, and burying our heads in the sand will not make it go away.

- The Great American Ponzi Scheme

- Quinn to receive Millions in Pensions Payments

- Taxpayers 7.65% Paycheck deductions and 7.65% employer contributions into Soc. Sec. and Medicare are Ponzi schemes too

No reasonable taxpayer would suggest that any public employee lose what they have personally contributed to their retirement, and that should never happen - just like it should never happen to taxpayers who have paid into the FEDERALLY REQUIRED ponzi scheme of social security and medicare their entire working lives. However, the idea of a lifetime "pension salary" for public employees is far fetched at this stage of State and community financial decay. It's fiscally impossible to cover all pension debts without collapsing every other system, industry and household in the State of Illinois. This State is in, what's considered by economists, a death spiral. Public pension and benefit systems need to be quickly amended and ultimately restructured into a fiscally responsible system - the same applies to social security too. Taxpayers know the feeling of retirement planning adjustments. Many taxpayers have been left with major losses after the economic collapse in 2008, and the collapse is still continuing now.

Obviously, the problem with pensions are all rooted in money - public employees are fighting to keep their generous pay and benefits and taxpayers are fighting to keep their taxes down and afford their bills. There is a common ground that can be reached, but it's up to public employees to work together and for the taxpaying citizens. Most taxpayers would not argue with public employees making an income consistent with local costs of living, contributing private sector rates to their health plan and contributing private sector rates to a defined contribution 401k-type retirement account. If this type of idea keeps getting fought by public employees, taxpayers' livelihoods will continue to be at stake as the tax burdens continue to fall solely on TAXPAYERS. This is where the hostility arises in these arguments. Most taxpayers savings, retirement accounts and lifestyles have all been diminished to afford the increasing cost of living and continually rising property taxes. Asking more from the taxpayers who are beyond financially extended to cover excessive costs of public salaries and benefits will never be met with acceptance. We understand the State did not contribute enough to the pension system, but the pension system ponzi scheme was never sustainable to begin with - its a ponzi scheme. It all looks good on paper, everyone involved in the pension ponzi knew what they wanted from it, but it was never sustainable. Public employees can blame the State, but Taxpayers blame all parties involved for agreeing to it, letting it continue, and causing it to directly affect us.

The fate of this State is going to come down greed or reason. We like to believe that public employees can reason on an acceptable resolution.

Restructure Benefits and Save Millions

Besides implementing the cost cutting measures described by this retired Board of Education member, here are some additional ideas that quickly add up to millions in savings:

RETIREMENT

Due to the structure and risk associated with defined-benefit (pension) plans, it is in the best interest of both the employee and the School systems (taxpayers) to instead utilize the defined-contribution (401k) type of retirement structure. Taxpayers are essentially funding all of the current "pension salaries" paid out to the employees for life, as the employee contributions cover such a small portion that it only lasts 20 months or so (depending on salary) of their pensions. Due mismanagement and impossible fiscal sustainability of defined-benefit pensions, the State should instead move public employees to a guaranteed and protected defined-contribution retirement system. It makes the most sense for both the employee and the taxpayer.

The current defined-benefit (pension) system looks like this: Lets hypothetically say a teacher makes $50,000 per year (a typical starting salary). They contribute 9.4% of their base salary to their pension, which is $4,700 per year. For simple math reasons, we'll say this teacher makes $50,000 per year for 30 years, contributing 9.4% of their salary to their pension. Over 30 years, this amounts to $141,000 that the teacher has contributed to their own pension. The teachers retirement system (TRS) pays a teacher 75% of the teacher's highest salary over the final 4 years of employment as a pension, for life. This teacher, who made $50,000 per year for 30 years will retire with a $37,500 pension salary per year for life... and the cost-basis break-even for this teacher will occur after 3.75 years. If this teacher retires at 55 years old and lives to be 85, taxpayers will end up covering 26.25 years of the retirement costs, or $984,375 (and this is NOT including the 3% cost of living increase compounded each year!). Imagine what the actual pensions equate to with the current salaries.